Research Brief

Economic Outlook

July 2026

Improving Economic Momentum

Supports Second-Half ’26 CRE Outlook

Labor market rebound points to optimism. Despite prolonged headwinds, recent job gains highlight the economy’s improving growth trajectory.

- The U.S. economy faced significant headwinds over the past 15 months, including tariffs, weak job creation, and geopolitical disruptions, all of which contributed to inflationary pressures.

- Despite this, overall economic performance has remained durable, signaling underlying resilience across key sectors.

- From May 2025 through February 2026, labor market conditions weakened, with a cumulative loss of nearly 50,000 jobs and reduced workforce mobility.

- Hiring activity shifted notably beginning in March 2026, with approximately 550,000 jobs added over the last four months, indicating renewed labor market momentum.

- Job growth has been concentrated in major metros — including New York, Dallas, Phoenix, Orlando, Los Angeles, and Houston — reinforcing demand for space across key CRE markets.

- If sustained, ongoing hiring and stable unemployment in the low-4 percent range would support CRE demand, particularly in apartments and office spaces.

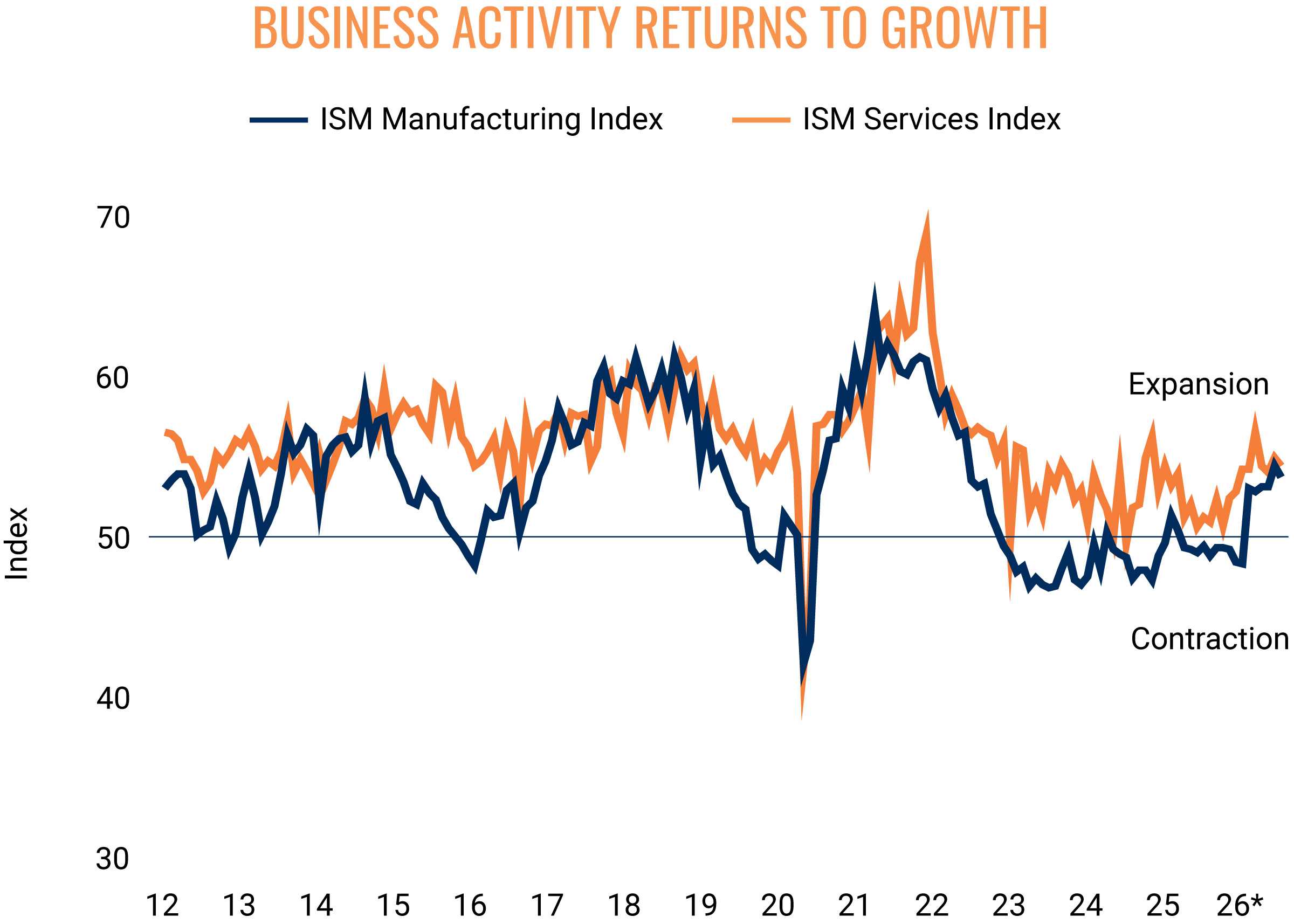

Business activity expands. Strengthening readings for manufacturing and business-services activity support increased demand for industrial and retail commercial real estate.

- Indexes from the Institute for Supply Management (ISM) Manufacturing and Services are signaling renewed economic expansion following a period of stagnation.

- The Manufacturing Index, which remained in contraction territory for much of the last year, has moved above 50 since January, indicating growth is returning.

- The Services Index has also strengthened, rising from near break-even levels to the mid-50s, signaling steady expansion across the 15-plus industries it tracks.

- ISM indicators have historically served as reliable signals of broader economic cycles.

- Continued momentum in these indexes supports a positive outlook for demand in industrial and retail real estate.

Consumption strength meets economic risks. Consumer resilience is supporting momentum, though risks tied to tariffs, inflation, and interest rates remain.

- Retail sales have emerged as a key pillar of economic resilience, with headline sales rising 6.9 percent year-over-year in May and core sales up 5.6 percent.

- On an inflation-adjusted basis, core retail sales increased 2.2 percent, indicating real growth in consumer spending.

- Despite concerns about elevated consumer debt levels, household debt service remains manageable at 11.2 percent of disposable income, 60 basis points below the pre-pandemic average for 2012-2019.

- Continued growth in retail sales supports sustained demand for retail and industrial CRE.

- Several risks remain, however, including ongoing tariff pressures and uncertainty surrounding the renegotiation of the United States-Mexico-Canada Agreement.

- Geopolitical instability, including a fluid situation in the Middle East, and an uncertain inflation outlook continue to pose potential challenges to sustained economic expansion.

- Financial markets are currently anticipating a 25-50 basis point interest rate increase by year-end, though easing inflation could reduce pressure on the Federal Reserve.

- Even with lingering headwinds, stable or modestly declining interest rates would support a favorable investment environment and reinforce improving CRE demand.

* Through June | Sources: Marcus & Millichap Research Services; Bureau of Economic Analysis;

Bureau of Labor Statistics; CME Group; Federal Reserve; Institute for Supply Management; U.S.

Census Bureau; U.S. Energy Information Administration

TO READ THE FULL ARTICLE