Research Brief

Inflation and Interest Rate Outlook

June 2026

CRE Outlook Favorable Despite Near-Term

Shifts in Energy Prices and Interest Rates

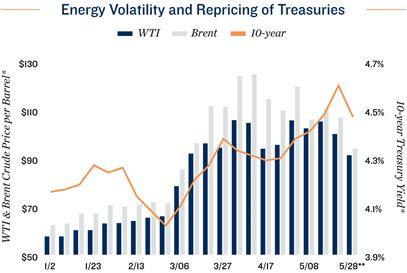

Energy markets get their bearings. Following initial volatility tied to geopolitical conflict, oil and fuel prices have begun to stabilize, supported by coordinated releases from reserves.

- Crude oil prices have not roamed substantially above $100 per barrel for prolonged periods, coming in lower than initial expectations following the onset of the Middle East Conflict.

- Coordinated releases from global emergency petroleum reserves have helped offset restricted shipping through the Strait of Hormuz.

- The U.S. Strategic Petroleum Reserve has declined materially, falling from roughly 415 million barrels before the conflict to about 375 million barrels by mid-May.

- About 10 million barrels per week are being drawn from the Strategic Petroleum Reserve, helping to moderate near-term energy price volatility.

- Gasoline prices appear to be settling around $4.50 per gallon nationally, while diesel is running near $5.60 per gallon, which continues to pressure transportation and distribution costs.

Inflation alters rate trajectory. Higher inflation readings have driven a reassessment of monetary policy expectations and bond yields, reshaping the broader interest rate environment.

- Elevated fuel costs are pushing inflation materially higher, with CPI inflation rising roughly 140 basis points since February to 3.8 percent in April.

- Upstream price pressures have accelerated sharply as PPI inflation climbed 260 basis points since February to 6.0 percent.

- The change in PCE has also moved higher, increasing from a 2.8 percent annual rise in February to the 4.0 percent range.

- As inflation expectations reset, markets have shifted from anticipating rate cuts in 2026 to pricing in a probability greater than 50 percent of a rate increase by year-end, driving Treasury yields higher.

- Since late February, the 5-year has risen to about 4.2 percent, while the 10-year has increased to the mid-4 percent range.

Long-term real estate dynamics improve. Near-term rate volatility may temper deal flow, but underlying market conditions support a constructive investment climate over the long run.

- While interest rate expectations have shifted higher, the policy outlook remains fluid, with potential de-escalation offering a path toward easing energy-driven inflation pressures.

- For CRE investors, the rapid rise in borrowing costs is the most immediate headwind, as deals that penciled earlier in the year have become more challenging.

- As a result, the bid-ask spreads between buyers and sellers are widening again, disrupting a market that had been moving toward greater pricing equilibrium.

- Despite interest rate volatility, substantial capital continues to target CRE, supported by the sector's inflation resistance and durability during economic slowdowns.

- Although borrowing costs are elevated, space demand remains sound while new supply pipelines continue to shrink, bolstering national rent growth in 2026.

* Average weekly value ** Data for the partial week ended 5/28

Sources: Marcus & Millichap Research Services; American Automobile Association; Bureau of

Economic Analysis; Bureau of Labor Statistics; CME Group; CoStar Group, Inc.; Federal Reserve;

Preqin; RealPage, Inc.; TradingEconomics; U.S. Energy Information Administration

TO READ THE FULL ARTICLE