Research Brief

Single-Family Housing Outlook

April 2026

Homeownership Trends Translate into Uneven CRE Effects

Higher rates reshape housing dynamics. Renewed inflation concerns and the Federal Reserve's delayed easing have increased mortgage rates, weighing on affordability, while home sales remain fairly steady.

- Geopolitical tensions raising oil prices, along with tariffs, have intensified inflation pressures, reducing the chances of near term expansionary monetary policy

- The Federal Reserve held interest rates steady in March, while market expectations have shifted markedly, with investors in early April assigning a 72 percent probability of rates remaining unchanged through December.

- Treasury yields have risen 30 to 50 basis points since late February as markets repriced the timing of rate cuts, contributing to elevated long-term financing costs

- Mortgage rates climbed 50 basis points, lifting the 30-year fixed rate to 6.46 percent, straining housing affordability.

- Higher mortgage rates have increased the average monthly payment on a median-priced home by $120 since late February

- Single-family home prices rose 0.2 percent over the past year, while sales volumes have remained stable near 4 million units annually since rate hikes began in 2022, roughly in line with early pandemic activity, but below long-run norms.

A softer housing market ripples across CRE. When homebuying slows, it can impact commercial property types tied to housing-related spending.

- Inflation-adjusted furniture sales declined 8.0 percent year-over-year through February, reflecting softer demand for home-related goods.

- Building and gardening sales increased 1.2 percent from last year, marking a modest improvement after more than three years of decline.

- Softer demand for home-related goods can modestly weigh on retail space demand, with marginal spillover effects on industrial space as retailers hold leaner inventories.

Affordability pressures favor multifamily. Cost barriers to homeownership and a sharp slowdown in construction are improving the long-term supply-demand balance for apartments.

- Rising mortgage payments and slower home sales have had the greatest impact on the multifamily sector.

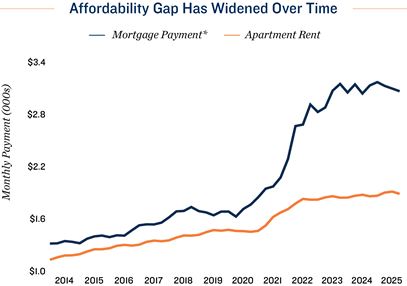

- Since the end of 2021, median home prices have risen more than 10 percent to approximately $420,000.

- Higher mortgage rates have lifted monthly payments on a median-priced home by more than 50 percent since 2021 to roughly $3,090

- During the same period, the average U.S. apartment rent has only risen about 13 percent to $1,854 per month

- The affordability gap between the average apartment rent and typical mortgage payment has widened to $1,236 per month, presenting a significant barrier for first-time homebuyers.

- Delayed transitions into homeownership have supported renter retention, with apartment renewal rates reaching 56 percent at the end of 2025.

- Elevated interest rates, tariff s, and shipping costs are further restraining multifamily construction, with starts down 72 percent from their 2022 peak and units under construction down 51 percent

* Mortgage payments based on median home price for a 30-year fi xed rate mortgage, 90% LTV, taxes,

insurance, and PMI; 27% mortgage payment coverage ratio

Sources: Marcus & Millichap Research Services; Bureau of Economic Analysis; Costar, Inc.; Federal

Reserve; Freddie Mac; Moody's Analytics; National Association of Realtors; RealPage, Inc; U.S.

Census Bureau

TO READ THE FULL ARTICLE