Research Brief

Canada Inflation

February 2026

Cooling Inflation Helps Clear Headwinds Facing

Canada’s CRE Market in 2026

Base effects mask further cooling. Inflation rose 2.3 per cent year over-year in January, down 10 basis points from December, and below expectations for an unchanged reading. On a monthly basis, prices were largely flat, underscoring the lack of meaningful momentum. As in prior months, distortions tied to last year’s temporary GST/HST holiday continued to affect the annual comparison. Previously tax-exempt items like restaurant prices surged 12.3 per cent year-over-year, while alcoholic beverages and children’s goods also posted outsized gains, reflecting base effects rather than fresh demand-driven pressures. These increases were more than offset by a 16.7 per cent annual decline in gasoline prices and moderating shelter costs. Excluding the impact of indirect taxes, year-over-year price growth slowed to 2.1 per cent, reinforcing that underlying inflation continues to cool.

Easing core pressures challenge prolonged policy restraint. The Bank of Canada’s preferred core measures — CPI-trim and CPI-median — rose at an average pace of just 0.11 per cent monthly, marking a third consecutive on-target gain and pulling the annual rate down 10 basis points to 2.5 per cent. While the base case still calls for rates to hold steady through year-end, evidence is mounting that inflation pressures may be overstated. Core disinflation is advancing faster than expected, hiring has softened — including January job losses — and fourth-quarter GDP growth now looks flat or slightly negative. Ongoing USMCA uncertainty is also weighing on business investment and consumer spending. Together, these trends could open the door to a potential rate cut if weakness persists.

Commercial Real Estate Outlook

Housing pressures ease as supply-demand dynamics shift. Shelter inflation continued to moderate in January, with costs rising 1.7 per cent year-over-year. Slower growth in both rent and mortgage interest costs drove the deceleration, reinforcing that housing-related price pressures are no longer intensifying. Notably, rent inflation cooled for a third consecutive month, falling 60 basis points to 4.3 per cent. This aligns with real-time multifamily fundamentals. National annual rent growth closed 2025 at 6.1 per cent, but further easing is expected through 2026 toward the mid-2 per cent range. A historic construction pipeline — with units under development at record highs — is expanding supply at the same time population growth is slowing under tighter immigration policies. Together, these forces are shifting leverage back toward renters, tempering what had previously been one of the most persistent sources of inflationary pressure.

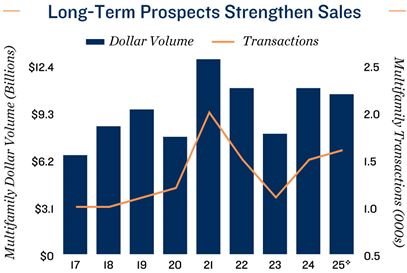

Apartment liquidity holds despite softer backdrop. Even as vacancy edges up and rent growth cools, multifamily investment remains resilient. The sector was the most liquid in 2025, accounting for roughly 35 per cent of dollar volume transacted nationally — the largest share among core commercial assets. While Alberta’s final figures are still pending, preliminary data indicates that transaction counts increased year-over-year, with total dollar volume appearing stable to modestly higher. This underscores that capital continues to target the sector, despite near-term operating softness. Investors are looking through cyclical challenges, focusing instead on long-term housing demand, improved rate clarity, and the defensive profile of rental assets.

* Through January; ** Forecast provided by Capital Economics; v Preliminary estimate

Sources: Marcus & Millichap Research Services; Altus Data Solutions; Canada Mortgage and

Housing Corporation; Capital Economics; CoStar Group, Inc.; Statistics Canada

TO READ THE FULL ARTICLE